The images from the streets of Chile have shocked the world over the last two weeks. This isn’t because people had a lot of money invested in Chile, but more because it is the wealthiest and until recently stablest country in the region. I tried my own explanation last week, and then published a follow-up after a lot of Chilean feedback.

Now, the question of exactly why Chile suddenly descended into disorder is gaining momentum. My colleague Tyler Cowen made his own attempt to explain what happened here, and greatly doubted that it could be attributed to inequality. As numerous Chileans have pointed out, inequality in the country has even been decreasing, albeit from excruciatingly high levels.

Explaining how this could happen becomes an urgent question for assessing risks almost everywhere else. And the more I look at it, the more it seems we need to invoke the nebulous Malcolm Gladwell concept of the “tipping point.” For whatever reason, Chilean opinion suddenly tipped. A rise in transport fares was the catalyst, but certainly not the underlying cause.

For a tipping point, just look at the president’s approval rating. It dropped steadily, and then collapsed. This is the latest poll from the Chilean pollster Plaza Publica. The purple line is for disapproval.

The same survey asked for opinions on the reasons for the disorder. The most popular response, mentioned by 41%, was “social discontent” — which begs many questions. “The cost of living” was next with 18%, while inequality was fifth, mentioned by only 12%. For even Chileans, then, it is unclear exactly why this trouble broke out, and why it broke out when it did.

I am planning to write more on this, and would greatly welcome feedback, particularly but not only from Chileans. Why exactly did this happen? The lack of a clear explanation is more unnerving for investors than anything else.

To close for now, I will mention one insight from Peter Atwater of Financial Insyghts, who makes a study of social mood and its effect on markets. He commented that neither the repo market meltdown of a few weeks ago, nor the sudden unrest in Chile, have yet been tagged with a clear explanation. “We don't like uncertainty to begin with, but uncertainty driven by unknown factors really makes us uncomfortable,” he said. “It raises randomness, which we abhor.”

The lack of narratives is alarming, and he suggests that another “event” without a clear explanation could set people even further on edge. So please, let us try to explain what happened in Chile.

...By the traditional metric of GDPper capita, the three cities are paragons of economic success.Per capitaincome is around $40,000 in Hong Kong, more than $60,000 in Paris, and around $18,000 in Santiago, one of the wealthiest cities in Latin America. In the2019 Global Competitiveness Reportissued by the World Economic Forum, Hong Kong ranks third, France 15th, and Chile 33rd (the best in Latin America by a wide margin).

Yet, while these countries are quite rich and competitive by conventional standards, their populations are dissatisfied with key aspects of their lives. According to the 2019 World Happiness Report, the citizens of Hong Kong, France, and Chile feel that their lives are stuck in important ways.

Each year, the Gallup Poll asks people all over the world, “Are you satisfied or dissatisfied with your freedom to choose what you do with your life?” While Hong Kong ranks ninth globally in GDP per capita, it ranks far lower, in 66th place, in terms of the public’s perception of personal freedom to choose a life course. The same discrepancy is apparent in France (25th in GDP per capita but 69th in freedom to choose) and Chile (48th and 98th, respectively).

...In all three countries, urban young people not born into wealth despair of their chances of finding affordable housing and a decent job. In Hong Kong, property prices relative to average salaries are among the highest in the world. Chile has the highest income inequality in the OECD, the club of high-income countries. In France, children of elite families have vast advantages in their life course.

... personal vehicles or public transport to get to work....thus be especially sensitive to changes in transportation prices

...ll three governments were blindsided by the protests. Having lost touch with public sentiment,

Crystals are orderly states of matter in which the arrangements of atoms take on repeating patterns. In the language of physics, they are said to have “spontaneously broken spatial symmetry.”

Time crystals, a newer concept, are states of matter whose patterns repeat at set intervals of time rather than space. They are systems in which time symmetry is spontaneously broken.

The notion of time crystals was first proposed in 2012, and in 2017 scientists discovered the first new materials that fully fit this category. These and others that followed offer promise for the creation of clocks more accurate than ever before.

...I must clarify what, exactly, a crystal is. The most fruitful answer for scientific purposes brings in two profound concepts: symmetry and spontaneous symmetry breaking.

In common usage, “symmetry” very broadly indicates balance, harmony or even justice. In physics and mathematics, the meaning is more precise. We say that an object is symmetric or has symmetry if there are transformations that could change it but do not.

...We say a law has symmetry if we can change the context in which the law is applied without changing the law itself. ...

...Time translation symmetry expresses a similar idea but for time instead of space. It says the same laws we operate under now also apply for observers in the past or in the future. In other words, the laws we discover at any time apply at every time.

...Without space and time translation symmetry, experiments carried out in different places and at different times would not be reproducible.

...Whereas ordinary crystals are orderly arrangements of objects in space, spacetime crystals are orderly arrangements of events in spacetime....We are looking, then, for systems whose overall state repeats itself at regular intervals.

...And that brings us to the lesson for today. On October 7, General Electric (GE)announcedseveral changes to its defined benefit pension plans. Among them:

Some 20,000 current employees who still have a legacy defined benefit plan will see their benefits frozen as of January 2021. After then, they will accrue no further benefits and make no more contributions. The company will instead offer them matching payments in its 401(k) plan.

About 100,000 former GE employees who earned benefits but haven’t yet started receiving them will be offered a one-time, lump sum payment instead. This presents employees with a very interesting proposition. Almost exactly like a Nash equilibrium. More below…

The first part of the announcement is growing standard. Employers prefer 401(k) plans because they transfer investment risk to the employees. Other than the matching payments—which end when the worker quits or retires—the company has no future obligations.

The second part is more interesting, and that’s where I want to focus.

Suppose you are one of the ex-GE workers (and I’ll bet I have some readers in that group) who earned benefits. As of now, GE has promised to give you some monthly payment when you retire. Say it’s $1,000 a month. What is the present value of that promised income stream? It depends on your life expectancy, inflation, interest rates and other factors. You can calculate it, though. Say it is $200,000.

Is GE offering to write you a generous check for $200,000? No. We know this because GE’s press release says:

Company funds will not be used to make the lump sum distributions. All distributions will be made from existing pension plan assets in the GE Pension Trust. The company does not expect the plan's funded status to decrease as a result of this offer. At year-end 2018, the plan's funded ratio was 80 percent (GAAP).

So GE is not offering to give away its own money, or to take it from other workers. It is simply offering ex-employees their own benefits earlier than planned. But under what assumptions? And how much? The press release didn’t say.

If that’s you, should you take the offer? It’s not an easy call. First, you are making a bet on the viability of General Electric. In September 2000, GE stock traded at $58+ per share. As I write this it is $8.45. The board has slashed dividends and the dividend yield is now only 0.47%.

As of April, GE had $92 billion in liabilities in its pension plan, on assets a little below $70 billion. Commendably, the company is “pre-funding” $4–5 billion into the DB plan. As we will see, however, this is chump change to the actual obligations.

In various ways, the choice GE pensioners face is one many of us will have to make in the coming years. GE isn’t the only company in this position. You’re still affected even if you don’t have a DB plan. Lots of people are reaching retirement age to find they only have 80% (and often less) of their “fully funded” amount. They have to fill the gap somehow. Most often, that means reducing expenses or working longer, if you’re able.

Life would be so much easier if we didn’t have to worry about our financial futures. Though I suppose we don’t have to worry. Animals don’t. Squirrels instinctively store away nuts and thus live through winter without much thought.

We humans have retirement winters, and we’re more sophisticated than squirrels. We generally outsource the job of managing our nuts/money to professionals. All well and good if we save enough and if the professionals do their jobs right. As we saw last week, the elected squirrels who run Social Security haven’t evolved to face changing conditions. Our Social Security nuts are in danger.

But the problem is even bigger. Today I want to continue this theme using some recent corporate news as our springboard. Economic changes have made future planning increasingly difficult for government retirement systems, private pension plans, and individual investors. How do you generate a reliable income stream for an uncertain but potentially lengthy lifespan in a world where interest rates are barely above zero and possibly below it?

The easy answer is “save more,” but that strategy has limits. We all have current expenses. Yes, we can live simpler lives, but we can’t save 100% of our income. Yet that’s what it will take in some scenarios.

If you’re starting to envy the squirrels, you aren’t the only one.

Remember “defined benefit” pensions? That is the kind of plan in which the employer guarantees the worker a set monthly benefit for life. They are increasingly scarce except for small closely held corporations. My US accountant has set up well over 1,000 defined benefit plans, including two for me. His primary customers are dentists. The same rules apply for small closely held businesses as for large corporations. These plans can be great tools for independent professionals and small business owners.

But if you have thousands of employees, DB plans are expensive and risky. The company is legally obligated to pay the benefits at whatever the cost turns out to be, which is hard to predict. The advantage is you can use some hopeful accounting to set aside less cash now and deal with the benefit problems later. The problem is “later” comes faster than you would like, and procrastination can be a bitch.

At some point, the risks outweigh the benefits, which is why few large companies have open DB plans these days. But the plans are often still in effect for older workers, and the amounts are large and frequently underfunded. Companies are slowly dealing with the problem.

And that brings us to the lesson for today. On October 7, General Electric (GE) announced several changes to its defined benefit pension plans. Among them:

Some 20,000 current employees who still have a legacy defined benefit plan will see their benefits frozen as of January 2021. After then, they will accrue no further benefits and make no more contributions. The company will instead offer them matching payments in its 401(k) plan.

About 100,000 former GE employees who earned benefits but haven’t yet started receiving them will be offered a one-time, lump sum payment instead. This presents employees with a very interesting proposition. Almost exactly like a Nash equilibrium. More below…

The first part of the announcement is growing standard. Employers prefer 401(k) plans because they transfer investment risk to the employees. Other than the matching payments—which end when the worker quits or retires—the company has no future obligations.

The second part is more interesting, and that’s where I want to focus.

Suppose you are one of the ex-GE workers (and I’ll bet I have some readers in that group) who earned benefits. As of now, GE has promised to give you some monthly payment when you retire. Say it’s $1,000 a month. What is the present value of that promised income stream? It depends on your life expectancy, inflation, interest rates and other factors. You can calculate it, though. Say it is $200,000.

Is GE offering to write you a generous check for $200,000? No. We know this because GE’s press release says:

Company funds will not be used to make the lump sum distributions. All distributions will be made from existing pension plan assets in the GE Pension Trust. The company does not expect the plan's funded status to decrease as a result of this offer. At year-end 2018, the plan's funded ratio was 80 percent (GAAP).

So GE is not offering to give away its own money, or to take it from other workers. It is simply offering ex-employees their own benefits earlier than planned. But under what assumptions? And how much? The press release didn’t say.

If that’s you, should you take the offer? It’s not an easy call. First, you are making a bet on the viability of General Electric. In September 2000, GE stock traded at $58+ per share. As I write this it is $8.45. The board has slashed dividends and the dividend yield is now only 0.47%.

As of April, GE had $92 billion in liabilities in its pension plan, on assets a little below $70 billion. Commendably, the company is “pre-funding” $4–5 billion into the DB plan. As we will see, however, this is chump change to the actual obligations.

In various ways, the choice GE pensioners face is one many of us will have to make in the coming years. GE isn’t the only company in this position. You’re still affected even if you don’t have a DB plan. Lots of people are reaching retirement age to find they only have 80% (and often less) of their “fully funded” amount. They have to fill the gap somehow. Most often, that means reducing expenses or working longer, if you’re able.

When GE says its plan is 80% funded under GAAP, it necessarily makes an assumption about the plan’s future investment returns. Here’s what they say in the 2018 annual report.

Source: GE

I dug around and found the “expected rate of return” was 8.50% as recently as 2009, when they dropped it to 8.00%, then 7.50% in 2014, to now 6.75%. So over a decade they went from staggeringly unrealistic down to seriously unrealistic. They still assume that every dollar in their pension fund will grow to almost $4 in 20 years.

That means GE’s offered amounts will probably be too low, because they’ll base their offers on that expected return. GE hires lots of engineers and other number-oriented people who will see this. Nevertheless, I doubt GE will offer more because doing so would compromise their entire corporate viability, as we’ll see in a minute.

In any case, more companies will do such things and affected workers won’t be happy. We’ll see the same in state and local government pensions, which are often even more underfunded and have even more absurd investment projections. These are becoming untenable and lump sum offers like GE’s help highlight that fact.

This, in turn, will raise pressure on plan sponsors to reduce those projections, which will increase the amounts they must contribute to their plans, which (for the corporate ones) will reduce earnings.

...All these cases have one thing in common, though: In each, Putin backed the status quo. Like the Russian czars of old, who saw it as their goal to support monarchies everywhere, he is a consistent opponent of regime change and backer of incumbents.

...Such a record endears Middle Eastern leaders to Putin: They can be reasonably certain he won’t pull a fast one on them. With the U.S. they can’t be so sure, since Washington has backed or directly performed several regime changes in the region.

...Middle East ... most of them, like Putin, are in charge of commodity-based economies.

...Putin’s Russia is not really a European, a Central Asian or an East Asian country, ... Its pivot to the Middle East is more natural than previous attempts to cozy up to the U.S. or the current overtures to China. Whether it’s in Russian national interests is a question for Putin’s successors to ponder.

Something’s happening to wages that neither Democrats nor Republicans care to acknowledge.

Stop me if this sounds familiar: For most American workers, real wages have barely budged in decades. Inequality has skyrocketed. The richest workers are making all the money. Earnings for low-income workers have been pathetic this entire century.

These claims help drive the interpretation of breaking economic news. For example, the Labor Department yesterday reported that the unemployment rate fell to a 50-year low, while wage growth stalled. “The wage numbers here are INSANE,” the MSNBC host Chris Hayes tweeted. “The tightest labor market in decades and decades and ordinary working people are barely seeing gains.”

So, let’s play a game of wish-casting.

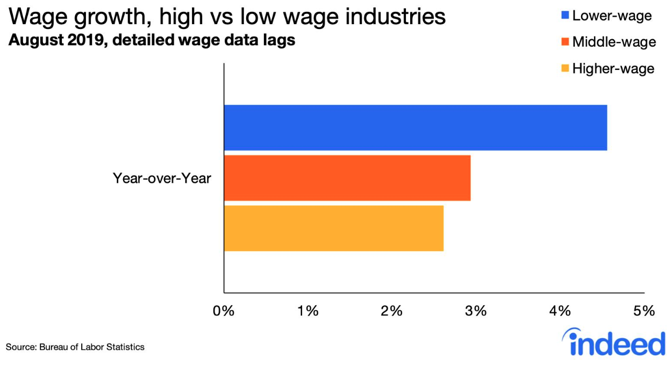

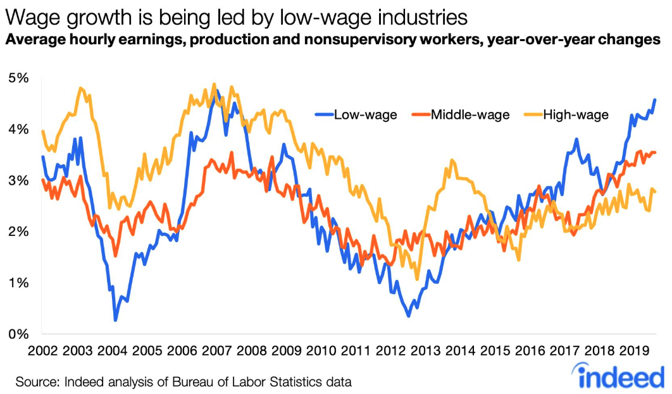

Imagine a world where wage growth was truly stagnant only for workers in high-wage industries, such as medicine and consulting.

Imagine a labor market where earnings growth for low-wage workers, such as those who work in retail and restaurants, had doubled in the past five years.

Imagine an economy where wages for the poorest Americans were rising twice as fast as hourly earnings for high-wage earners.

It turns out that all three of those things are happening right now.

According to analysis by Nick Bunker, an economist with the jobs site Indeed, wage growth is currently strongest for workers in low-wage industries, such as clothing stores, supermarkets, amusement parks, and casinos. And earnings are growing most slowly in higher-wage industries, such as medical labs, law firms, and broadcasting and telecom companies.

Bunker’s analysis is not an outlier. A Goldman Sachs look at data from the Bureau of Labor Statistics found growth for the bottom half of earners at its highest rate of the cycle. And even among that bottom half, the biggest gains are going to workers earning the least. A New York Times analysis of data from the Federal Reserve Bank of Atlanta found that wage growth among the lowest 25 percent of earners had exceeded the growth in every other quartile.

In fact, according to Bunker’s research, wages for low-income workers may be growing at their highest rate in 20 years.

What’s happening here? Donald Trump hasn’t sprinkled MAGA pixie dust over the U.S. economy. In fact, his trade war has clearly diminished employment growth in industries, that are sensitive to foreign markets, such as manufacturing. Rather, a tight labor market and state-by-state minimum wage hikes have combined to push up wage growth for the poorest workers. The sluggishness of overall wage growth is concealing the fact that the labor market has done wonderful things for wages at the low end.

One reason you haven’t heard this economic narrative may be that it’s inconvenient for members of both political parties to talk about, especially at a time when economic analysis has, like everything else, become a proxy for political orientation. For Democrats, the idea that low-income workers could be benefiting from a 2019 economy feels dangerously close to giving the president credit for something. This isn’t just poor motivated reasoning; it also attributes way too much power to the American president, who exerts very little control over the domestic economy. Meanwhile, corporate-friendly outlets, such as TheWall Street Journal’s editorial pages, have reported on this phenomenon. But they’ve used it as an opportunity to take a shot at “the slow-growth Obama years” rather than a way to argue for the extraordinary benefits of tight labor markets for the poor, much less for the virtues of minimum-wage laws.

Democrats don’t want to talk about low-income wage growth, because it feels too close to saying, “Good things can happen while Trump is president”; and Republicans don’t want to talk about the reason behind it, because it’s dangerously close to saying, “Our singular fixation with corporate-tax rates is foolish and Keynes was right.”

But good things can happen while Trump is president, and Keynes was right. “Tighter labor markets sure are good for workers who work in low-wage industries,” Bunker told me. “This recovery has not been spectacular. But if we let the labor market get stronger for a long time, you will see these results.”

Why It’s So Hard for Startups to Create Wealth in Europe

Lawmakers across the Continent haven’t given startups the compensation tools they need to share profits with employees. That’s changing.

By

Edward Robinson

From

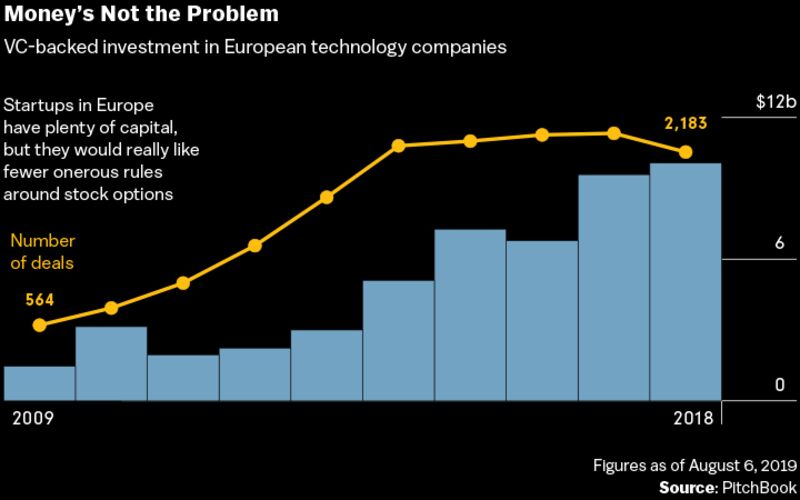

Johannes Reck should be feeling pretty groovy. He’s the co-founder of one of the hottest startups in Berlin. GetYourGuide lets holiday makers book tours online in 150 countries and is on course to increase ticket sales this year by 75%. In May it raised $484 million from investors, and it’s now valued at more than $1 billion.

Reck’s company is precisely the type of unicorn European policymakers want to see more of as they champion entrepreneurship that can kick-start much-needed economic growth. But he’s fuming. “It’s not even that I am disappointed—I am angry, really angry, because you don’t need to reinvent the wheel here,” says Reck, a 34-year-old German with the wiry build of a marathoner. “It’s not like we are asking politicians to do something unheard of.”

Illustration: Jaya Nicely for Bloomnberg Markets

The problem? Reck can’t provide his people with a stake in the future of their venture without incurring crushing costs and hassle. For decades, tech mavens in the U.S. have used stock options for employees to spur innovation—and unprecedented wealth. Unlike Silicon Valley, where equity incentive plans have become as ubiquitous as foosball tables and midday yoga sessions, the options culture has yet to take root in many European countries. While some lawmakers are taking action to loosen restrictions on pay, it’s going to be hard to close the gap when income inequality is becoming a more urgent issue on both sides of the Atlantic.

European consumers and lawmakers here have long decried outsize paydays as unfair and vulgar. A few years ago the Dutch capped bonuses for bankers, money managers, and other financial professionals at 20% of their base salaries. Entrepreneurs must navigate onerous tax rates and restrictions that often make equity sharing and options more trouble than they’re worth. When employees in Germany exercise options, they have to pay income tax on the difference between the fair market value and the strike price, and that rate runs from 14% to 47.5%. They also have to pay a 25% capital-gains tax on additional profits when they sell their shares.

In contrast, American employees typically pay a 0% to 20% rate on capital gains when options are redeemed, though they may have to pay additional levies when they’re exercised, depending on the timing and the type of equity incentive program. Germany and 14 other countries, including Sweden and the Netherlands, are more burdensome than the U.S. regarding options, according to a 2018 study by Index Ventures, a venture capital firm in London and Silicon Valley.

For entrepreneurs and venture capitalists, the problem isn’t just about attracting top talent. The compensation bind may also be a big reason why Europe doesn’t produce world-beating tech companies at the same level as the U.S.

Other forces are at work, too. Even though they’re part of the European Union, member states remain a fragmented collection of markets that can’t muster the borderless scale achieved in America. Plus, there’s the widely shared belief that European business culture simply doesn’t tolerate the experimentation and inevitable failures that are par for the course in, say, Silicon Valley. While governments across the EU have devoted hundreds of millions of euros to venture capital-style programs to invest in startups, the one tool entrepreneurs truly want remains out of reach.

“There are two ingredients to growth in a startup,” says Martin Mignot, an Index Ventures partner. “One is capital, and the other is talent, and when you’re not highly profitable you have to incentivize employees on the promise of the upside. Your currency is that promise.”

Spotify, Klarna, and TransferWise lead a roster of European companies that have shaken up industries with new products and created wealth for their investors and employees. Likewise, a handful of countries hew to the American approach on compensation; Britain, Italy, Portugal, and, interestingly enough, France, tax options as capital gains when they’re cashed in.

Yet they’re the exceptions. In many other European markets, startup founders have to use various workarounds to vest employees in their businesses. In Sweden, options can be taxed as income at rates of more than 50%. Klarna, a digital payments powerhouse, sidesteps the bill by issuing warrants priced at fair market value using the Black-Scholes model, which are taxed as capital gains at 25% to 30% at the time of sale. But, as incentives, fully priced warrants aren’t as potent as cheaper priced options, says Knut Frangsmyr, Klarna’s chief operating officer. Companies in Austria, the Czech Republic, Germany, and Spain distribute “virtual share options,” but the instruments are really just cash bonuses by another name and may not deliver the windfalls that bona fide options do when a company is acquired or holds an initial public offering.

In Germany, at least, help may finally be on the way. Bettina Stark-Watzinger, chairwoman of the Finance Committee in the Bundestag, Germany’s parliament, has crafted legislation that would cut the tax rate on stock options in half by treating them as capital gains instead of income. Stark-Watzinger, a member of the centrist opposition Free Democratic Party, argues that Germany has become complacent about supporting digital innovation.

She worries that promising tech companies will decamp to other countries if lawmakers don’t change things. “We are so preoccupied with the economy of the last century,” Stark-Watzinger says in her office suite near Berlin’s iconic Brandenburg Gate. “We are so proud of our trade surplus and our automobile industry, but we have fallen behind in the digital economy. This is where value and growth will come from in the future.”

VC-backed investment in European technology companies

It won’t be easy for Stark-Watzinger to persuade parties in Germany’s governing coalition to embrace legislation that might be seen as favoring workers in the relatively well-off tech sector. Germany has been far less comfortable than the U.S. and the U.K. about carving out exceptions in its tax system for specific sectors, even to stimulate innovation, says Michael Mandel, an economist at the Progressive Policy Institute in Washington who has studied the issue. It wasn’t until this year that the German government proposed a tax break for research and development investments across industries, a common policy in many Western countries.

Whenever the issue of tax credits has come up in the Bundestag, lawmakers have tended to question whether lower revenue will undermine support for social services—a political third rail in a nation that provides free tuition at public universities an VC-backed investment in European technology companies

It won’t be easy for Stark-Watzinger to persuade parties in Germany’s governing coalition to embrace legislation that might be seen as favoring workers in the relatively well-off tech sector. Germany has been far less comfortable than the U.S. and the U.K. about carving out exceptions in its tax system for specific sectors, even to stimulate innovation, says Michael Mandel, an economist at the Progressive Policy Institute in Washington who has studied the issue. It wasn’t until this year that the German government proposed a tax break for research and development investments across industries, a common policy in many Western countries.

Whenever the issue of tax credits has come up in the Bundestag, lawmakers have tended to question whether lower revenue will undermine support for social services—a political third rail in a nation that provides free tuition at public universities and universal health care.

Mandel says that just because Washington is willing to bet that forgoing tax revenue now will result in bigger inflows later, that doesn’t mean Berlin should. “Germany has a very successful industrial system, so why should they break something that’s working?” he says. “And while German leaders would love to have more unicorns, they might want to develop them their way, not the Silicon Valley way.”

Even so, there’s little doubt that stock options have fueled wealth and innovation in the U.S. Companies such as PayPal Holdings Inc., the online payments pioneer, haven’t just made their founders wildly rich; members of the so-called PayPal mafia like Elon Musk, Peter Thiel, and Reid Hoffman went on to start ventures that minted fortunes for rank-and-file employees who can then start their own companies and begin the cycle anew.

Index’s Mignot calls this the flywheel effect. The flywheel isn’t nonexistent in Europe: The 2018 IPO of Adyen, a Dutch digital payments processing company, made its top brass billionaires. Yet reforming options rules across the EU would help make creating such flywheels the norm instead of the exception, says Magnus Henrekson, the director of the Research Institute of Industrial Economics in Stockholm. At the top of the reform list is making sure beneficiaries aren’t hit with taxes until gains are realized.

GetYourGuide’s Reck, for one, is relieved the issue is finally on the agenda. In many respects, his company looks like a classic Valley performer. It’s backed by SoftBank Vision Fund, and in September it moved its headquarters into a renovated electrical substation that’s a model of post-industrial hipness, with exposed red brick walls, cast-iron beams, and fridges stocked with high-caffeine Club-Mate drinks.

Even though Reck was determined to add the pièce de résistance—options—he gave up after realizing that the upfront tax bill would empty workers’ pocketbooks. So he implemented ersatz shares that are essentially cash awards tied to GetYourGuide’s valuation.

Those payouts are taxed as income, but only when they’re redeemed, and there’s no capital-gains tax. But GetYourGuide, which isn’t profitable yet, must reserve cash to cover the outlays. “This has massive disadvantages for the company,” says Reck. “We have a huge liability on our balance sheet toward employees, which is obviously weird. And in an IPO scenario, this is something that you have to explain to investors, and that’s not great.”

Raisin, another startup, did bite the bullet, granting stock options to its employees. Located in Prenzlauer Berg, a Berlin neighborhood of funky cafes and old Soviet-style apartment buildings, Raisin runs an online “deposit marketplace” that matches European savers with banks offering the best interest rates. Backed by Goldman Sachs Group Inc. and PayPal, it’s invested €16 billion ($17.7 billion) in assets.

Frank Freund, Raisin’s co-founder and chief financial officer, isn’t wild about requirements that date to a bygone era. Whenever Raisin grants shares, a notary must literally read the lengthy compensation agreement aloud to both the employee and Freund at a hearing that can take up to 90 minutes. Still, Freund believes the company made the right call. “When you have participation in the company’s performance and growth, it makes a big difference,” he says. “It would be great if significantly more companies would follow our example in Germany.”

Scott Chacon will take a pass on that. Chacon is an American entrepreneur who co-founded the software development site GitHub Inc. He’s been spending time in Berlin with his latest venture, an online language-tutoring service called Chatterbug Inc. Following a panel discussion, he mingles with local techies over beers in a leafy courtyard outside a VC firm.

Amid the bonhomie, he says Chatterbug chose to base itself in San Francisco and Berlin to tap into the German capital’s diverse expatriate pool. It offered employees a choice of U.S.-style options or German-style virtual shares. But ensuring the different programs were equitable was impossible. Chatterbug now offers new employees restricted stock units that aren’t pegged to a strike price (as options are) and are taxed as income if they’re cashed in during a sale of the company.

Standing alongside Chacon, Anne Leuschner, the company’s COO, chimes in. She says Chatterbug’s compensation fudge isn’t ideal, but it’ll do for now. “I wish we had the same system as the U.S.,” she says. “But they don’t want us to get rich in Germany.”

Robinson covers wealth in London. With Birgit Jennen