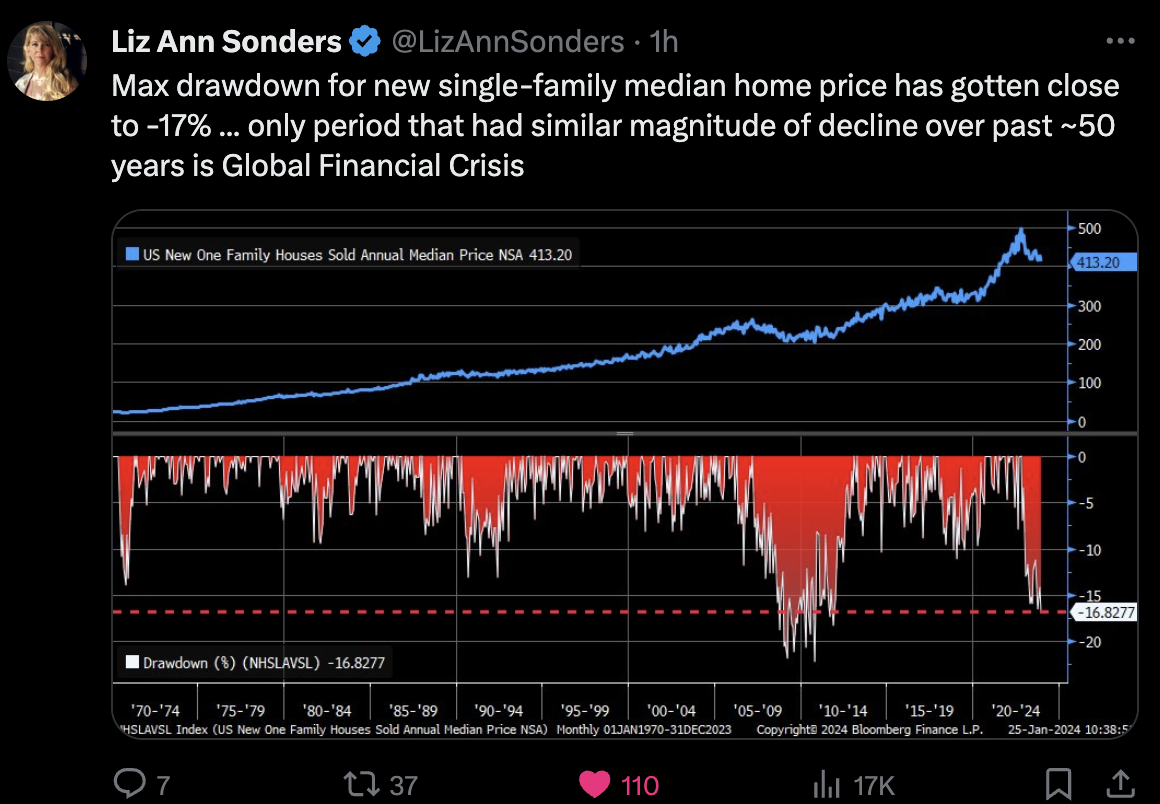

Higher mortgage rates have cooled new buying activity almost everywhere. Some areas are in better shape than others. The commercial office space situation, however, is another story. Today's subprime-like problem? Possibly. We'll look deeper into it today. But first, back to the conference in Tampa.

Four different real estate funds presented. One invests in existing multi-family and student housing. They buy, manage, fix up the units, and increase the rents with the goal of exiting their properties at a higher price. Buy, fix, improve, sell. Two of the funds develop real estate. The fourth fund is creating an entirely new real estate investment category in the vein of professionally managed Airbnb vacation rentals. These properties generate considerably more cash flow than traditional home rentals. Hearing this piqued my interest.

It wasn’t just the subject matter of the presentations that was interesting. The format of the due diligence meeting allowed attendees to pepper the presenters with questions. There were some very smart people in the room, and their questions made for quite a fun, Shark Tank–like atmosphere.

I was mainly interested in understanding the source of each fund’s debt, financing costs, loan timelines, the willingness of their banks to lend, and other potential stress points.

My high-level takeaways are that, at the moment, capital is more difficult to obtain but not impossible. Banks have cut back the amount of money they’re willing to lend. The typical loan-to-value (LTV) ratio is 40– 50%, which is down from 60–75%. That's a material change. Think of it this way: If you were looking to buy a multi-family apartment building for $1 million a year ago, banks would have lent you up to 75% of the cost, or $750k. Today, they will only lend you 50%, or $500k.

Overall, because interest rates are higher, debt costs are also higher, and while the funds can find additional sources of debt, they come at much higher lending rates. Higher funding costs combined with lower lending ratios logically decrease potential returns. Gone are the hot returns of the zero-interest-rate-policy days, but the market generally looks to be in okay shape. The key to the equation is available liquidity within the banking system, and that's where the problems in the commercial office space could come into play.

Bad stuff happens when the leverage ratio gets too high while property values decline. That's the problem in the commercial office market today. Loans are coming due, and since many companies moved to partially or fully remote workforces in the pandemic and, therefore, left office spaces empty, property values have come way down. As you saw in the 60 Minutes video report shared in last week's post, there’s a massive supply of unrented office space. Rents support a landlord's ability to stay current on their loans. Refinancing them is an issue for both the landlords and the banks.

Is this impacting banks’ willingness and/or ability to lend? Yes, and we are just in the early innings. And this can spillover to all other areas that require bank financing and to the boarder economy.

In last week's OMR, I raised the question of whether or not this will be “the Next Big Short.” By that, I’m, of course, referring to 2008, when Wall Street guru Michael Burry realized that a number of subprime home loans were in danger of defaulting. Burry bet against the housing market by throwing over $1 billion of his hedge fund money into credit default swaps on subprime mortgage loans. Think of them like put options; you make money when the price drops. He and several others made a fortune from the economic collapse. The crisis put Lehman Brothers out of business and sent then–Treasury Secretary and former Goldman Sachs Chairman and CEO Hank Paulson to legislators begging for a banking bail-out. Great leverage can cause great problems.

So, are we on the doorstep of another Big Short? The answer lies in the banking system and the backstops that legislators and the Fed may or may not provide to the system. The office rental woes are real. The uncertainties are the value of the underlying collateral, the level of bank exposure, and the ability of landlords to refinance their debts. Personally, I don’t believe this is as big of a problem as the subprime junk that avalanched the banking system in 2008, and the Fed and legislators have proven they are willing to be shockingly creative, but the risk to the banking system is not immaterial. We will go deeper into the issue today, concluding next week with a piece that gives us a sense of the size of the exposure within the system.

Grab that coffee and find your favorite chair. I'm going to share some notes from my conversations with a former banker–turned–real estate investor and another developer friend from the Northwest. He’s been sounding the alarm bell for several months and says what we’ll see next is “jingle mail"—like the sound the keys make in the envelope sent from the property owners to their banks.

You'll find a few telling charts as well, and we’ll look at the cyclical trend in the S&P 500 Index and the 10-year Treasury Yield. Finally, don't miss this week's Random Tweets section. Thanks for reading. It’s time to hit the send button… I’m heading home “to let the night sky touch my soul”… alongside my beautiful wife, Susan. Wishing you and your loved ones the very best. |

No comments:

Post a Comment